Here are the benefits and requirements for suspending your social insurance benefits. You can suspend social security benefits for a variety of reasons. Your situation will determine which reason you choose. You will need to apply for benefits at full retirement age if you are married. Your situation will be even more complicated if you have minor children.

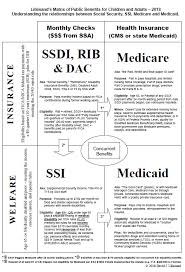

Suspension of Social Security

Social Security benefits can be suspended by the Social Security Administration for several reasons. The reasons can range from the beneficiary's age and life expectancy to their pay history. The suspension of benefits may last for months or even years depending on the case. It may be considered a delay if the suspension lasts for a prolonged period.

The death of a spouse is one reason why a delayed benefit may be granted. This means the widow cannot receive the survivor advantage on her record. The widow can build delayed credits up to 70 years old.

Requirements

When a Social Security beneficiary decides to suspend their benefits, there are certain requirements that must be met. Section 202(z), the Social Security Act, outlines the rules for the suspension. This section contains information about the rules of voluntary suspension, unsuspension or reinstatement benefits. To apply for reinstatement, beneficiaries must wait 180 days from the date of suspension.

One common reason for a person to suspend their benefits is increased income from outside sources. This could mean increased part time work or taxable pension accounts. This could lead to fluctuations in Social Security benefits and may result in a tax bill.

Benefits

There are two main strategies for delaying Social Security benefits. The file-and-suspend strategy is for married couples. It allows one spouse to claim spousal benefits, while the other continues to delay individual retirement benefits. Both spouses will earn delayed retirement credits as the other spouse continues to defer his or her benefits. This strategy is sometimes effective but not for everyone.

Another option is to stop receiving your retirement benefits when you reach full retirement age. When you suspend your benefits, your benefit will start at a higher value than it would have been had you waited until full retirement age. This option will allow you to use delayed retirement credits to increase your benefit. If you had started receiving benefits at age 62 your benefit would have been reduced 30% and your delayed retirement credits would have been used to reduce the benefit.

Prices

Before you decide to suspend your Social Security benefits, it is important that you understand the financial implications. For starters, you have to consider whether you'll have more income from other sources after the suspension. If you do, you will have to pay taxes on any income received from outside government sources. You must also ensure that your outside income exceeds 50% of your Social Security benefit. This means that you will need to make $25,000 a calendar year if a single person, and $32,000 for married people.

If you file a claim too early, you'll be required to pay an additional 25% per month in benefits. Your total benefit will then be slightly less than $11,100. The amount you receive if your benefits are suspended for more than four years will increase by 32% (or about $336 each month). This means that your monthly benefit for 70 years will be $1386/month (adjusted according to inflation).

When should it be done?

Consider suspending your Social Security Benefits if you need extra cash. This will allow for you to pay your bills until your benefits resume. Additionally, you'll earn delayed retirement credits, which will boost your benefit eventually by two-thirds of a percent for every month or year that you're off the rolls. There are a few things that you should know before making the decision.

First, you need to consider the tax implications of suspending Social Security Benefits. The federal government might require you to pay income taxes on Social Security benefits if your income exceeds certain thresholds.

FAQ

How to manage your wealth.

To achieve financial freedom, the first step is to get control of your finances. It is important to know how much money you have, how it costs and where it goes.

You must also assess your financial situation to see if you are saving enough money for retirement, paying down debts, and creating an emergency fund.

If you fail to do so, you could spend all your savings on unexpected costs like medical bills or car repairs.

What is estate planning?

Estate Planning refers to the preparation for death through creating an estate plan. This plan includes documents such wills trusts powers of attorney, powers of attorney and health care directives. The purpose of these documents is to ensure that you have control over your assets after you are gone.

Who can I turn to for help in my retirement planning?

Many people consider retirement planning to be a difficult financial decision. This is not only about saving money for yourself, but also making sure you have enough money to support your family through your entire life.

Remember that there are several ways to calculate the amount you should save depending on where you are at in life.

For example, if you're married, then you'll need to take into account any joint savings as well as provide for your own personal spending requirements. If you are single, you may need to decide how much time you want to spend on your own each month. This figure can then be used to calculate how much should you save.

You could set up a regular, monthly contribution to your pension plan if you're currently employed. Consider investing in shares and other investments that will give you long-term growth.

These options can be explored by speaking with a financial adviser or wealth manager.

What is retirement plan?

Retirement planning is an important part of financial planning. It helps you plan for the future, and allows you to enjoy retirement comfortably.

Retirement planning includes looking at various options such as saving money for retirement and investing in stocks or bonds. You can also use life insurance to help you plan and take advantage of tax-advantaged account.

How to Select an Investment Advisor

It is very similar to choosing a financial advisor. Two main considerations to consider are experience and fees.

An advisor's level of experience refers to how long they have been in this industry.

Fees are the price of the service. It is important to compare the costs with the potential return.

It's crucial to find a qualified advisor who is able to understand your situation and recommend a package that will work for you.

Do I need to pay for Retirement Planning?

No. This is not a cost-free service. We offer free consultations that will show you what's possible. After that, you can decide to go ahead with our services.

Who Should Use A Wealth Manager?

Anyone who is looking to build wealth needs to be aware of the potential risks.

It is possible that people who are unfamiliar with investing may not fully understand the concept risk. As such, they could lose money due to poor investment choices.

People who are already wealthy can feel the same. Some may believe they have enough money that will last them a lifetime. But they might not realize that this isn’t always true. They could lose everything if their actions aren’t taken seriously.

Therefore, each person should consider their individual circumstances when deciding whether they want to use a wealth manger.

Statistics

- According to a 2017 study, the average rate of return for real estate over a roughly 150-year period was around eight percent. (fortunebuilders.com)

- Newer, fully-automated Roboadvisor platforms intended as wealth management tools for ordinary individuals often charge far less than 1% per year of AUM and come with low minimum account balances to get started. (investopedia.com)

- US resident who opens a new IBKR Pro individual or joint account receives a 0.25% rate reduction on margin loans. (nerdwallet.com)

- If you are working with a private firm owned by an advisor, any advisory fees (generally around 1%) would go to the advisor. (nerdwallet.com)

External Links

How To

How to beat inflation with investments

Inflation is one important factor that affects your financial security. Inflation has been steadily rising over the last few decades. There are many countries that experience different rates of inflation. India, for instance, has a much higher rate of inflation than China. This means that even though you may have saved money, your future income might not be sufficient. You could lose out on income opportunities if you don’t invest regularly. How should you handle inflation?

Stocks can be a way to beat inflation. Stocks have a good rate of return (ROI). You can also use these funds to buy gold, silver, real estate, or any other asset that promises a better ROI. However, before investing in stocks there are certain things that you need to be aware of.

First, determine what stock market you wish to enter. Do you prefer small or large-cap businesses? Decide accordingly. Next, consider the nature of your stock market. Do you want to invest in growth stocks or value stock? Make your decision. Finally, understand the risks associated with the type of stock market you choose. There are many stocks on the stock market today. Some stocks can be risky and others more secure. Make wise choices.

You should seek the advice of experts before you invest in stocks. They can help you determine if you are making the right investment decision. Diversifying your portfolio is a must if you want to invest on the stock markets. Diversifying will increase your chances of making a decent profit. If you invest only in one company, you risk losing everything.

If you still need assistance, you can always consult with a financial adviser. These professionals will guide you through the process of investing in stocks. They will guide you in choosing the right stock to invest. You will be able to get help from them regarding when to exit, depending on what your goals are.